Reveals About Emerging Companies

In today’s markets, how a management team speaks is as consequential as what it delivers. Consistent, disciplined communication has emerged as a leading — and often underpriced — signal of long-term value creation.

COMMUNICATION AS A STRATEGIC ASSET

In public markets, communication is no longer a quarterly formality; it is a strategy. For every earnings call, investor presentation, and management commentary filed on the exchange, institutional participants are running a parallel analysis that goes far beyond the headline numbers. They are assessing whether the people running the business actually understand it, can articulate it with clarity, and are willing to be honest about where it is going.

This scrutiny has intensified as institutional participation in small and mid-cap companies has accelerated. Capital that once flowed exclusively to large-cap certainty is now actively seeking growth in the SME and emerging-company segment, but with a sharper governance lens. The result: management quality is increasingly visible not just in financial disclosures but also in the quality of the communication that surrounds them.

Management quality is often first visible in communication discipline — long before it

shows up in operating metrics.

What this signals is a fundamental shift in how value is being assessed. The old model, buy the numbers and ignore the narrative, is no longer sufficient. In an environment where earnings call transcripts are parsed algorithmically and investor presentations are benchmarked quarter over quarter, the communication layer has become a critical input into valuation.

WHY EMERGING COMPANIES FACE GREATER SCRUTINY

The dynamics are particularly acute for companies in the growth and emerging phase. These businesses lack the decade-long track records that allow institutional investors to build conviction from historical data alone. In the absence of established operating history, messaging becomes the proxy. It becomes the fastest-available signal of strategic clarity, internal alignment, and execution confidence.

An established company can survive a bad quarter with intact credibility. An emerging company that delivers a bad quarter and communicates it poorly, vague on reasons, silent on remediation, and defensive on guidance faces a disproportionate reset in how the market prices its future. The asymmetry is real, and it disproportionately punishes businesses that have not invested in communication discipline.

The real differentiator, then, is not whether a company can deliver growth but whether the management team can communicate the context, constraints, and trajectory of that growth in a way that builds durable investor confidence.

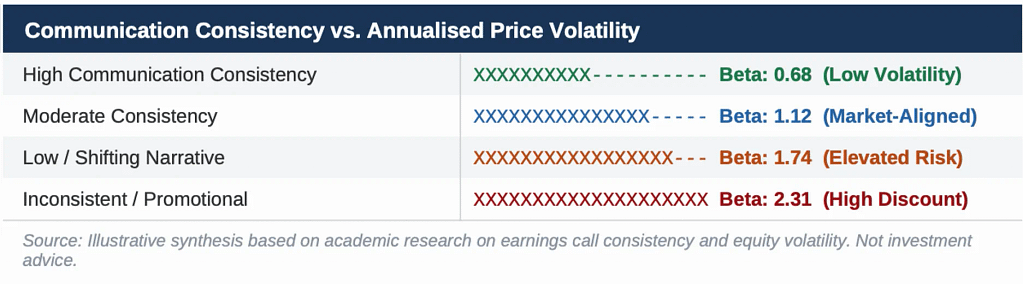

CHART 1 — Communication Consistency vs. Stock Volatility

THE COST OF INCONSISTENT COMMUNICATION

Markets punish confusion faster than they punish underperformance. This is a counterintuitive but empirically observable pattern. A company that misses its guidance but communicates the miss clearly with candour about the drivers and a credible path forward often retains more market confidence than one that surprises positively but communicates erratically.

The specific behaviours that erode trust are well-documented. Changing narratives across consecutive quarters where a growth strategy described confidently in Q1 is quietly repositioned by Q3 signals either a lack of strategic conviction or a management team managing perception rather than execution. Overly optimistic guidance that consistently falls short creates a credibility deficit that is difficult to reverse once established.

The valuation consequences compound over time. Analysts apply higher discount rates to businesses where guidance reliability is low. Institutional investors with fiduciary mandates actively avoid companies where the communication record suggests information asymmetry. The result is a persistent valuation discount that has nothing to do with underlying business quality and everything to do with how management has chosen to communicate.

|

Markets are increasingly rewarding companies where there is a disciplined, auditable alignment between what management says and what the business delivers.

|

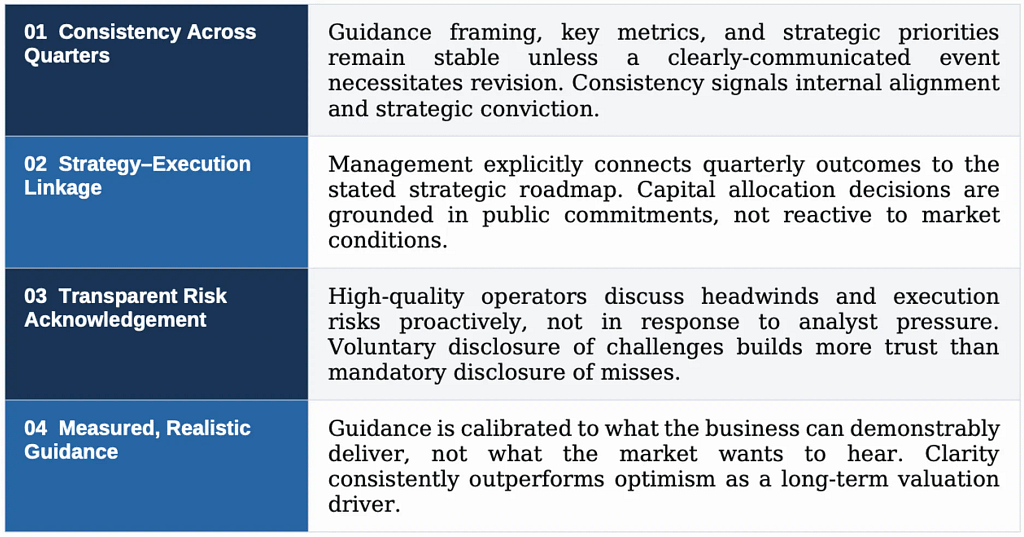

FOUR TRAITS OF HIGH-QUALITY MANAGEMENT COMMUNICATION

Across emerging companies that have successfully built institutional following, four communication traits consistently appear:

THE COMMUNICATION–EXECUTION FLYWHEEL

There is a compounding dynamic that sophisticated investors learn to identify early. Strong communication builds investor trust. That trust translates into patience during execution cycles, the willingness to hold through a difficult quarter without triggering a disorderly sell-off. When execution follows through on the communicated roadmap, credibility deepens further.

Over time, communication discipline compounds into a valuation premium. Companies that have consistently aligned their messaging with their delivery trade at higher multiples do so not merely because of their financial performance, but because the market has priced in the reliability of their future communication. The optionality embedded in trusting management is real, and it has measurable financial value.

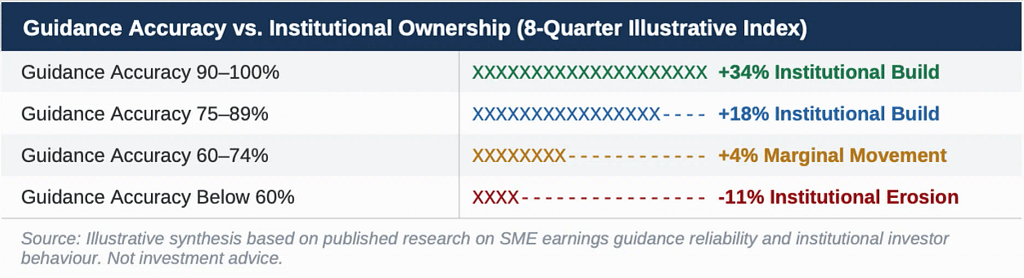

CHART 2 — Guidance Accuracy vs. Institutional Confidence

WHY THE MARKET IS RAISING THE BAR

The standards applied to emerging company communication have permanently shifted upward. Several structural forces are driving this change. Institutional capital targeting the small and mid-cap segment now demands governance standards that were, until recently, the preserve of large-cap firms. Quarterly earnings calls, investor days, and structured management presentations, once optional exercises, are increasingly viewed as baseline expectations. Simultaneously, the information infrastructure around public companies has democratised. Earnings call transcripts, investor presentation archives, and regulatory filings are now systematically indexed, analysed, and compared. Narrative inconsistencies that might have gone unnoticed in an earlier era are surfaced within hours of a filing. Narratives are audited in real time.

For management teams in the emerging company segment, this means that communication is not a communications function; it is a governance function. The way a company chooses to speak to its market participants is now a direct input into how it is valued, how it attracts capital, and how it is perceived as a long-term steward of investor resources.

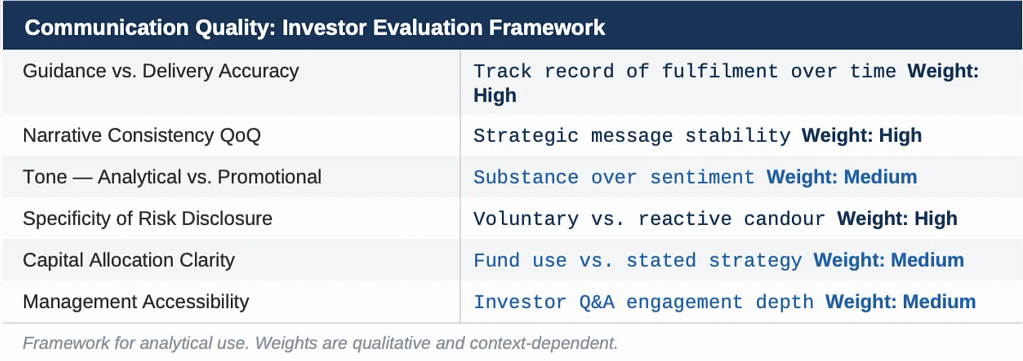

AN INVESTOR FRAMEWORK: EVALUATING COMMUNICATION QUALITY

For institutional participants and serious market analysts, a structured approach to evaluating communication quality has emerged as a practical differentiator. In today’s market, communication is a form of execution, and it can be assessed with similar rigour.

CHART 3 — Communication Quality Evaluation Framework

The practical application is straightforward: compare what management said twelve months ago against what has been delivered and what is being said today. Where the linkage is tight, the communication quality score is high. Where there is drift in framing, in metrics prioritised, or in guidance philosophy, that drift is itself an investable signal.

THE NEW COMPETITIVE ADVANTAGE

As more emerging companies enter public markets and as institutional capital deepens its reach into the small and mid-cap segment, the pressure on management teams to communicate with precision and consistency will only intensify. The winners in this environment will not be defined solely by operational excellence or product-market fit; they will be defined by their ability to translate that excellence into a communication record that markets can trust.

This is not about investor relations as a marketing discipline. It is about building an institutional-grade track record of saying what you will do and doing what you say. The companies that internalise this as a governance imperative, not a quarterly afterthought, will carry a structural advantage in cost of capital, analyst coverage quality, and institutional ownership stability.

|

In the long run, trust is built not just on results but on how consistently and honestly those results are communicated.

|

For founders, management teams, and board members navigating this environment, the message is unambiguous: your communication record is being audited every quarter, and it is being priced every day. In today’s market, communication discipline is not a soft skill — it is a hard competitive advantage._